Photos and infographs by Kelly Rodriguez

Sophomore Isabel Cornavaca works twice as hard to maintain her credit score after she made a big purchase in the first few months of having a credit card.

Cornavaca, who works at Sephora and the Pepperdine Volunteer Center, said that even when she transfers an extra $100 to her credit card account, it still “doesn’t make a dent” to fix her credit score. She attributes her situation from a lack of education in money management.

“My credit score suffered because I spent $500 on a haircut in Beverly Hills and my credit limit was $700 when I first got my card,” Cornavaca said.

Senior Steven Garcia said he feels less stress about maintaining his personal budget but tries not to think about his student loan debt.

“I postpone thinking about my student loan debt except for when the FAFSA application time comes,” Garcia said. “Besides that, I purposefully don’t think about it.”

Many college students in America are apprehensive about personal finance management, which includes managing credit card and student loan debt. According to a 2015 study by EverFi and HigherOne, 12 percent of student respondents said they never check their bank balances because they are too nervous. In contrast, only 58 percent of students from four-year institutions said they felt prepared to manage their money.

With percentages of debt in America increasing, college students’ anxiety about money management continues to increase as well. Armed with passion to fight that battle, both students and university innovators are trying to provide resources for students to prevent financial problems and set students on a path toward financial literacy and well-being.

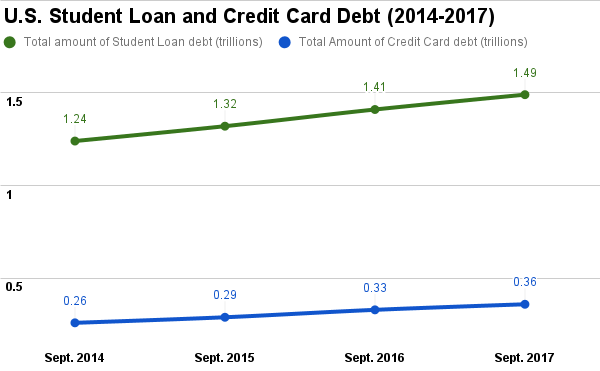

Source: U.S. Federal Reserve

Ignorance Isn’t Bliss

Eighteen to 34-year-olds were more likely to engage in “expensive credit card behaviors” than any other age category, according to a 2013 study from the FINRA Investor Education Foundation. Similarly, a 2015 study from the Global Financial Literacy Excellence Center showed that college students that borrowed loans “did not fully comprehend what they were taking on” when they got their loans. Fifty-four percent said they did not try to figure out how much their monthly payments would be.

Paul Goebel, the director of the Money Management Center at the University of North Texas, said in his experience, students often don’t understand the scope of personal finance issues.

“In 2017, there’s still such a stigma toward money management,” Goebel said in a phone interview. “Students don’t want to recognize that they need to manage their finances. Then what’ll happen is that a problem will quickly escalate into a crisis.”

Director of the Pepperdine Office of Financial Literacy and five-year MBA alumnus Derek Stoutland (‘16) said student aversion to personal finance development can be attributed to fear.

“It’s easy to say, ‘I’m just bad with finances and that’s how it’s just gonna be,’” Stoutland said. “In that case, it’s the fear talking: ‘I don’t wanna face this because it sounds intimidating, so I’m not gonna look at my finances.’”

Here to Help

Since its creation in 2005, the Money Management Center at the University of North Texas has become well-known in financial education circles for not only its commitment to providing resources for college students, but for the amount of student engagement they see every year.

The center offers three programs, according to Goebel. The Financial Readiness program, which focuses on student outreach through events and class presentations, sees 10,000 to 12,000 students yearly. The Financial Wellness program, which handles student coaching and financial assessments for students, sees 3,000 to 4,000 students yearly. The Financial Support program, which provides alternate loan programs for students at the University of North Texas, sees 1,500 to 2,000 students yearly.

Goebel said the success of the center rests in its ability to provide financial resources to different types of students.

“Financial literacy means different things to different people,” Goebel said. “Any financial literacy program needs to address the proactive student seeking to be more diligent with their budget and the reactionary student in crisis mode looking for options. One size does not fit all.”

Stoutland said Pepperdine’s Office of Financial Literacy has used the University of North Texas as an example in creating their own program for financial literacy.

Stoutland, with the help of Controller of the Pepperdine Finance Office Brian Thomason, created the Financial Literacy Initiative.

Stoutland said the process started with a submission for a Waves of Innovation grant in spring 2015. Stoutland and Thomason originally pitched the idea to Waves of Innovation II as a website with resources for Pepperdine students. Through the process, Stoutland was encouraged to expand upon his original idea. The “Financial Literacy Initiative” became a three-year plan to offer financial literacy courses and create an office. The idea was selected as a finalist and subsequently won.

“[Waves of Innovation II] was a process of being able to relate to other students and learning to provide resources for anyone at Pepperdine,” Stoutland said.

Now in its third year of operation, the office has been transitioning out of its status as a Waves of Innovation recipient to a standalone, fully-funded office. In their two full years of operation, they have offered events, convocations, workshops and classes for students to learn more about personal finance.

Financial Literacy Classes

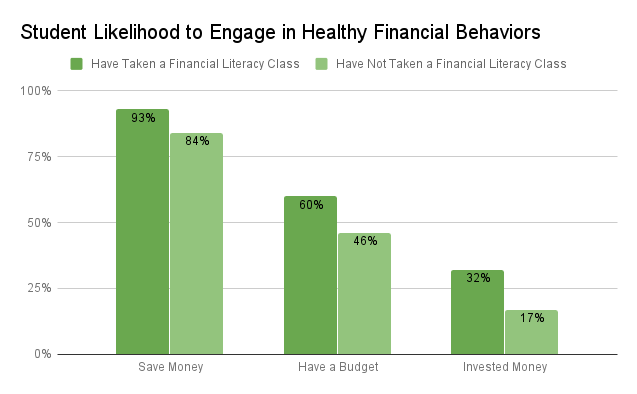

Research has shown that financial literacy classes increase the likelihood of student engagement. Students who took a class in personal finance were more likely to engage in financially responsible behaviors like saving, budgeting and investing than their peers that did not take the class, according to a 2016 report from the Council for Economic Education.

Source: Council for Economic Education

In 2013, California enacted AB166, which requires that grades 7 through 12 integrate “financial preparedness” into curriculum. However, the bill states that California doesn’t have an “official statewide policy or educational plan for the teaching of financial literacy” which means that some middle and high schools might not integrate financial literacy in a measurable way. This could also mean that California middle and high school students would not be prepared for managing finances in college.

Junior Courtney Ruud-Johnson didn’t have a finance class in high school and was not exposed to it before she got to Pepperdine.

Ruud-Johnson’s was in the first offering of the first semester of the First Year Seminar class, “Money Management for Millennials,” offered by the Office of Financial Literacy in fall 2015.

“Everyone in the class had the seminar as their top choice,” Ruud-Johnson said. “People were really involved and interested in the class.”

Ruud-Johnson said the class focused on researching and writing papers about different money management topics like budgeting and credit cards each week.

“We’d look for resources and talk about them in class,” Ruud-Johnson said. “If we wanted to use the research we found on opening a credit card account, we could use the information we found for class. It was super useful.”

The class’s curriculum has evolved with each iteration due to student feedback via surveys, Stoutland said.

“We’ve been surveying them and seeing students have a stronger understanding of personal finance in general [from the class] but also more of a desire to keep pursuing [financial education],” Stoutland said.

J.D. Schleppenbach, who works as the director of Fiscal and Administrative Services at the School of Law, is teaching the seminar for the first time this semester. Previous teachers were Thomason and Chris Bauman, who is the budget director for the Graziadio School. Schleppenbach said he expanded upon past curricula by bringing in more speakers.

“I used my contacts to have a lot of guest speakers come in,” Schleppenbach said. “It’s very valuable to get more voices in.”

Freshman Christopher Hidalgo, who was put in Schleppenbach’s class this semester, said the class inspired him change his major.

“I was a Biology major before this class,” Hidalgo said. “I switched to an Accounting major because I wanted to learn more about finance.”

The seminar class also succeeded in engaging Ruud-Johnson, who now works with the Office of Financial Literacy.

Stoutland said the office also offered a personal finance elective in the business division that was open to all students during its first year. But, the class hasn’t been offered since Spring 2016 because it hasn’t found a professor whose schedule would be able to fit the class.

“The interest is there and the curriculum is there, but it’s about finding the right professor,” Stoutland said.

Student-Run Finance Clubs

Goebel said the Money Management Center has thrived on student initiatives.

“Social media for [the center] is dynamic because our student workers own it,” Goebel said. “Students want to listen to and learn from other students.”

Pepperdine’s Office of Financial Literacy ran a Personal Finance club at the beginning of the initiative’s launch. However, Ruud-Johnson said a lack of student engagement kept it from meeting like a traditional club this year.

“We had 30 students the first year, but with the way Pepperdine works, they all went abroad last year,” Ruud-Johnson said. “I was the only original person that stayed.”

Ruud-Johnson said that this year, the Personal Finance Club doesn’t meet, but it exists between the students that work with the office.

Meanwhile, another student-run finance-oriented club has started this semester.

Seniors Sloan Madoff and Connor McFarland saw a need for more advanced student engagement in the financial world. Together, they created and set up The Wave Pool: Student Investment Club, which aims to provide a place for students to practice investment portfolio management.

Madoff said that the club is structured in a way where students can come in and learn about investing then practice it.

“The first goal of the club is to lecture to the group on a holistic view of investing and on how to build a repeatable process,” Madoff said. “The second goal is to make it a functional environment where students build teams and investment theses.”

While they provide a brief overview of personal finance and financial literacy, Madoff said their goal is not to spend time talking about personal finance. However, Madoff said that there is room to collaborate with the Office of Financial Literacy for personal finance events for the student body.

Madoff and McFarland said that like the Office of Financial Literacy, they want to increase student awareness and engagement with finance as a whole.

“We want to make finance known at Pepperdine,” McFarland said. “Then we want Pepperdine to make waves in the finance industry.”

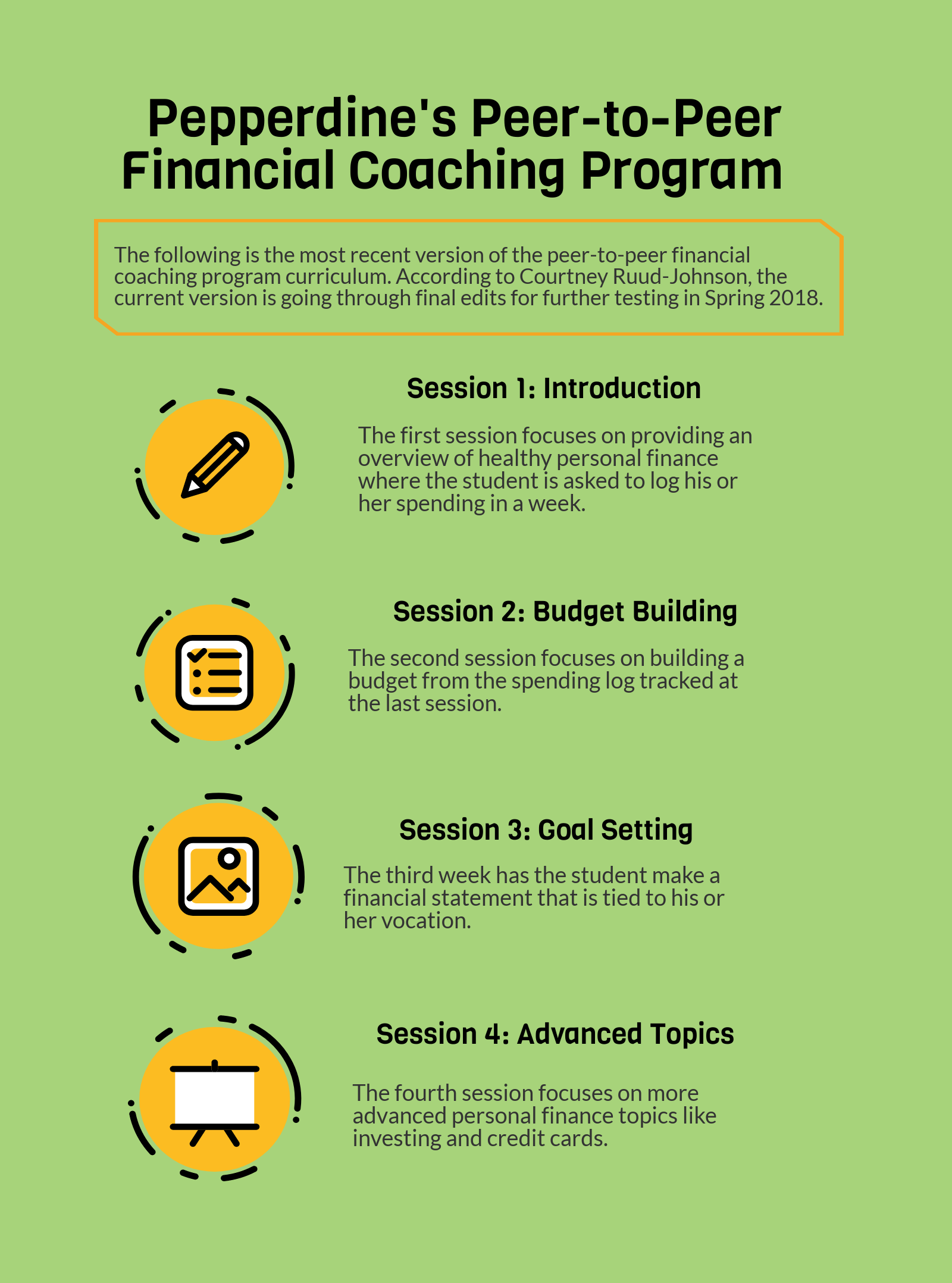

The Office of Financial Literacy has also been “beta testing“ a peer-to-peer financial coaching program, according to Stoutland.

“[We’ve developed] a short curriculum for any student who’s interested, regardless if they’re a business or finance major,” Stoutland said.

“The curriculum is based on other schools and we’re doing lots of surveys to figure out what topics are most of interest,” Ruud-Johnson said.

Before becoming a coach herself, Ruud-Johnson was one of the first “test subjects” for the program. So far, the program has been tested by five students, all of which have been part of the Personal Finance club.

The program is not officially on campus yet because the office is still improving it, according to Ruud-Johnson.

“We’ve been working on refining it this semester,” Ruud-Johnson said. “It’s in its final round of edits, so we’re hoping to do more testing next semester.”

Evaluation

Overall, the programs that exist at Pepperdine to increase student engagement with personal finance education are still in their early stages, so they can’t be properly evaluated. Currently, each program’s goals are to increase their own awareness before they can establish themselves as students’ go-to resource.

According to Stoutland, the Office of Financial Literacy needs to increase awareness and funding before they build a brick and mortar space.

“As of right now, it’s kind of like a ghost operation,” Stoutland said. “There’s no physical establishment yet at Pepperdine.”

The office currently exists in promotional efforts such as convocations, speakers and International Programs workshops. If a space were to open up, Stoutland said that the Career Center has offered a place for the peer-to-peer coaching sessions.

“It’s a long term goal to have a specific spot on campus where students can work to understand personal finance,” Stoutland said.

Stoutland added that he is fundraising to aid further efforts for the office.

The first-year seminar class, meanwhile, seeks to capture the attention of Pepperdine freshmen, but Ruud-Johnson said if it were to become a general education requirement, that it would need to be opened up to more students.

Schleppenbach also said that more could be done to engage other students that wouldn’t be able to take the first year seminar.

“We’re doing our students a disservice if we’re allowing them to pull out the amount of debt they’re pulling out for college and not teaching them how it works,” Schleppenbach said.

That, perhaps, creates a space for the peer-to-peer coaching program. But, because the program is still in its early stages of development, its effectiveness cannot be fully discussed.

Ruud-Johnson said that from her experience, the interest for peer-to-peer coaching is there.

“I’ve had so many friends ask me for help with budgets,” Ruud-Johnson said. “I’m hoping we can open a space for peer-to-peer mentoring.”

Stoutland said he and the office are committed to creating a place at Pepperdine where students can reframe their approach to personal finance.

“I want Pepperdine to be a financial literacy hub in America,” Stoutland said.

Stoutland added that financial literacy is not a “one and done thing.”

“It’s a lifetime process. You’re not immediately dubbed financially savvy and you move forward with your life,” Stoutland said. “It’s a constant battle.”

What resources have been most helpful in building good financial habits? What do you wish Pepperdine could offer to help teach financial literacy? Share your opinions in our comment section below!

________________

Follow Kelly Rodriguez on Twitter at @KRodrigNews